Algorithmic trading — using predefined rules (algorithms) to buy and sell assets. Come to think of it, when a caveman picked up a stick and rolled a huge boulder off the path — that’s also an algorithm: “If rock blocks path в†’ pick up stick в†’ roll rock.”

Why this matters:

Algorithms free you from emotions, save time, and allow 24/7 trading. In crypto, this is especially important: the market never sleeps, but humans do.

What is an Algorithm in Simple Terms

Algorithm — step-by-step instructions to achieve a goal.

Real-life examples:

-

Borscht recipe:

- If you have beets в†’ grate them

- If no meat в†’ add beans

- Cook for 2 hours в†’ serve with sour cream

-

Getting ready for work:

- If alarm rings в†’ get up

- If raining в†’ take umbrella

- If traffic jam в†’ turn on navigator

Trading algorithm:

- If price crosses moving average from below в†’ buy

- If price drops 5% from high в†’ sell

- If time is 18:00 в†’ close all positions

History of Trading Algorithms

Pre-computer Era: Paper Rules

1920s: Jesse Livermore (legendary trader) uses “trading rules.”

His algorithm:

- If stock rises 3 days in a row в†’ buy

- If drops 10% from peak в†’ sell

- If news is bad в†’ reduce position

Result: One of the largest fortunes of the time ($100+ million), several bankruptcies due to violating his own rules among other factors.

Lesson: Algorithm works only if you follow it.

1950-1970: First Computers

1950s: Computers appear on Wall Street.

First algorithms:

- Calculating moving averages

- Simple conditions: “If MA(50) > MA(200) в†’ buy”

Problem: Room-sized computers, expensive, slow.

1971: NASDAQ — first electronic quotation system.

- Quotes on screens (not phone calls)

- But trading still by phone (market makers in offices)

- Fully electronic trading: late 1980s (SOES after 1987 crash)

Important: NYSE still used “open outcry” trading. NASDAQ was an alternative, but not a fully automated exchange in the modern sense.

1980-1990: Quantitative Analysis

1980s: Quant funds appear.

Renaissance Technologies (Jim Simons):

- Mathematicians, physicists, astronomers instead of traders

- Algorithms based on statistics, patterns

- Returns: 66% annually (1988-2018)

Lesson: Math beats intuition.

1990-2000: High-Frequency Trading (HFT)

1990s: Internet, fast computers.

HFT (High-Frequency Trading):

- Thousands of trades per second

- Profit from microscopic price differences

- Requires: direct connection to exchange, servers near exchange

HFT peak: 2000-2010.

- 60-70% of trading volume in US

- Scandals: Flash Crash 2010 (1000-point drop in minutes)

2010-2020: Cryptocurrencies and Retail Bots

2010: Bitcoin starts trading on exchanges.

Crypto market features:

- 24/7 (no weekends)

- High volatility (±10% per day — normal)

- Many exchanges (arbitrage opportunities)

2015-2020: Bots for retail traders.

- 3Commas, Cryptohopper, HaasOnline

- Ready strategies: DCA, Grid, Trailing Stop

- Accessible to everyone ($20-100/month)

2020-2026: AI and Machine Learning

2020s: Neural networks in trading.

What AI can do:

- Analyze news (NLP — natural language processing)

- Recognize patterns on charts (CNN — convolutional networks)

- Optimize strategy parameters (RL — reinforcement learning)

Problem:

- AI requires data (years of history)

- AI doesn’t understand “black swans” (unpredictable events)

- AI can overfit (works only on historical data)

Important: Using ready-made “AI bots” from marketplaces is often a marketing gimmick. Training models requires data scientist qualifications, not just parameter tweaking.

Conclusion: AI is a tool, not a magic wand.

Types of Trading Algorithms

1. Trend Strategies

Idea: “The trend is your friend.”

Algorithm:

- If price above MA(50) and MA(200) в†’ long

- If price below MA(50) and MA(200) в†’ short

- If MAs cross в†’ exit

Example:

- BTC rises from $60,000 to $100,000 (6 months)

- Algorithm bought at $65,000, sold at $95,000

- Profit: +46%

Pros:

- Catches big moves

- Simple logic

Cons:

- Loses in sideways (frequent false signals)

- Lag (enters late)

2. Counter-Trend Strategies

Idea: “What goes up must come down.”

Algorithm:

- If RSI > 70 (overbought) в†’ short

- If RSI < 30 (oversold) в†’ long

- If RSI normal в†’ wait

Example:

- BTC dropped from $100,000 to $80,000 in a day

- RSI = 25 (strong oversold)

- Algorithm bought at $80,000, sold at $90,000

- Profit: +12.5%

Pros:

- Works in sideways

- Fast trades

Cons:

- Dangerous in strong trend (can catch a falling knife)

- Requires precise entry points

3. Arbitrage (for Advanced)

Idea: “Buy cheap on one exchange, sell expensive on another.”

Algorithm:

- If BTC on Bybit = $95,000, and on Binance = $95,300

- Buy on Bybit, sell on Binance

- Profit: $300 (minus fees)

Reality for retail trader:

- Price difference between major exchanges: 0.1-0.3% (rarely more)

- Opportunities disappear in milliseconds (HFT competition)

- For capital < $10,000, arbitrage is practically inaccessible

- More realistic: futures arbitrage (basis trading), pair arbitrage

Pros:

- Low risk (market doesn’t matter)

- Predictable profit (if you made it)

Cons:

- Need capital on two exchanges

- Fees eat profit

- Competition with HFT (need low latency)

- Not recommended for capital < $10,000

4. Market Making

Idea: “Profit from the spread (difference between buy and sell).”

Algorithm:

- Place limit buy at $94,900

- Place limit sell at $95,100

- Spread: $200

- If both sides executed в†’ profit $200

Example:

- Spread: 0.2-0.5%

- Volume: $1,000,000/day

- Profit: $2,000-5,000/day (minus risks)

Rebates:

Exchanges pay makers for providing liquidity. Maker fee is often negative (e.g., -0.005% to -0.025%), meaning you get paid for placing limit orders.

Pros:

- Profit in any market

- Exchanges pay rebates

Cons:

- Risk of one-sided position (price moved, order stayed)

- Requires constant monitoring

- Need large capital for noticeable profit

5. DCA (Dollar Cost Averaging)

Idea: “Buy regularly, regardless of price.”

Algorithm:

- Every Monday buy $100

- Doesn’t matter if price is $50,000 or $100,000

- Averaging entry price

Example:

- Week 1: $100 / $50,000 = 0.002 BTC

- Week 2: $100 / $60,000 = 0.00167 BTC

- Week 3: $100 / $55,000 = 0.00182 BTC

- Total: $300 / 0.00549 BTC = $54,645 average price

Pros:

- вњ… No emotions

- вњ… Volatility averaging

- вњ… Suitable for long-term investments

Cons:

- вќЊ Doesn’t maximize profit (could have bought at the bottom)

- вќЊ Requires discipline

6. Grid Trading

Idea: “Place a grid of orders within a range.”

Algorithm:

- Range: $90,000-100,000

- Grid step: $1,000

- Place 10 buy orders ($90k, $91k, … $99k)

- Place 10 sell orders ($91k, $92k, … $100k)

- If price oscillates в†’ profit on each cycle

Example:

- Price: $95,000 в†’ $96,000 в†’ $95,000 в†’ $96,000

- Bought at $95k, sold at $96k в†’ +$1,000

- Repeated 10 times в†’ +$10,000

Pros:

- вњ… Works in sideways (70% of the time)

- вњ… Automatic, 24/7

Cons:

- вќЊ Dangerous in trend (price exited range)

- вќЊ Requires large capital (many orders)

- вљ пёЏ Important: If price exits the range, the bot may end up with a full bag of losing assets (bought everything, didn’t sell).

Algorithms on Traditional Markets vs Crypto

| Parameter | Traditional Markets | Crypto Markets |

|---|---|---|

| Trading hours | 9:30-16:00 (exchange hours) | 24/7 |

| Volatility | 1-3% per day | 2-10% per day (depends on asset and market phase) |

| Fees | 0.01-0.1% | 0.02-0.1% |

| Leverage | Up to 100x (futures) | Up to 125x (crypto exchanges) |

| Regulation | SEC, CFTC, strict rules | Weak (depends on jurisdiction) |

| HFT | 60-70% of volume | 20-50% of volume (estimates vary, exact data is proprietary) |

| Accessibility | Qualified investors | Anyone with internet |

Conclusion: Crypto is more accessible, more volatile, but riskier. HFT share in crypto is estimated at 20-50% for centralized exchanges (CEX), but exact data is proprietary.

How to Create Your First Algorithm

Step 1: Choose a Strategy

Questions:

- What’s my capital? ($100, $1,000, $10,000)

- How much time do I have? (full-time, 1 hour/day, once a week)

- What risk is acceptable? (1%, 5%, 10% of capital)

Recommendations:

- Capital < $1,000: DCA, Grid (low fees)

- Capital $1,000-10,000: Trend, counter-trend

- Capital > $10,000: Arbitrage, market making

Step 2: Define Rules

Template:

IF [entry condition] в†’ THEN [action]

IF [exit condition] в†’ THEN [action]

IF [risk condition] в†’ THEN [action]Example (trend):

IF price > MA(50) AND MA(50) > MA(200) в†’ BUY

IF price < MA(50) в†’ SELL

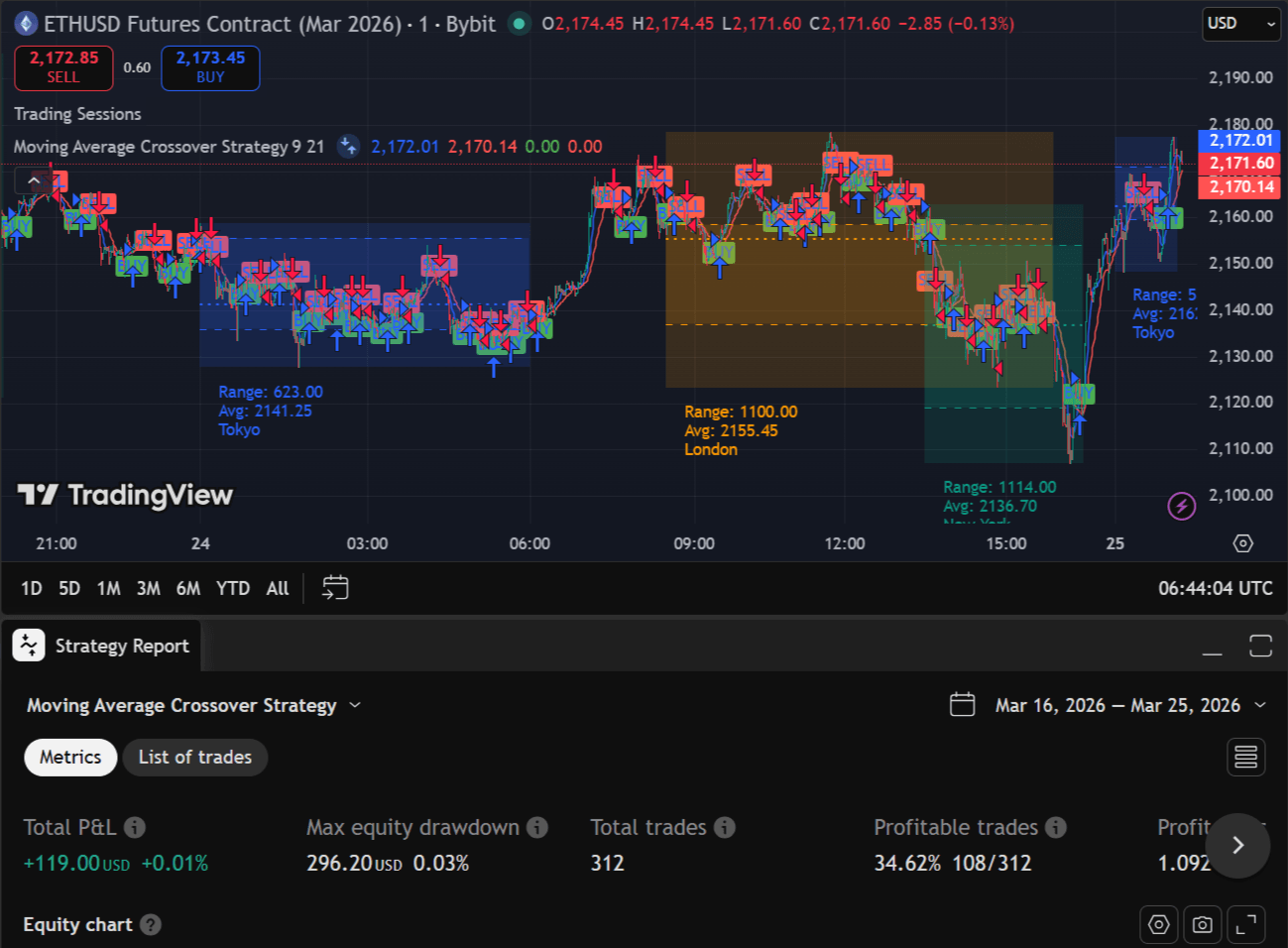

IF loss > 5% в†’ STOP-LOSSStep 3: Backtest on Historical Data

Backtest — testing a strategy on historical data to evaluate performance.

Tools:

MT4/MT5 Terminals:

- MQL4/MQL5 language

- Built-in strategy tester

- Expert Advisors (automated strategies)

- Pros: Powerful, many ready solutions

- Cons: Forex/CFD only, paid licenses

TradingView:

- Pine Script language

- Simple syntax (5-10 lines for basic strategy)

- Built-in backtester

- Pros: Free, many cryptocurrencies, cloud-based

- Cons: Limited logic vs Python

Python Libraries:

- Backtrader, Freqtrade, CCXT

- Pros: Full freedom, free

- Cons: Need coding, setup

Ready Platforms:

- Veles: Crypto algo trading, backtests, cloud bots — try Veles (affiliate link)

- Gainium: Grid, DCA, market making (free up to 2 bots)

- 3Commas: DCA, Grid, Trailing

- Antbot: Copy trading, signals

- Ginarea: Visual strategy builder focused on futures

What to check:

- Returns (% per period)

- Drawdown (max peak-to-trough drop)

- Number of trades (statistical significance)

- Win rate (% of profitable trades)

Step 4: Launch with Real Money

Rules:

- Start small (10% of capital)

- Monitor first trades

- Keep a journal (why entered, why exited)

- Don’t change algorithm after 1-2 losing trades

Step 5: Analyze and Optimize

Metrics:

- Sharpe Ratio: Return / risk (good > 1)

- Max Drawdown: Maximum drop (good < 20%)

- Profit Factor: Profit / Loss (good > 1.5)

- Win Rate: % of profitable trades (good > 50%)

Important: Don’t over-optimize!

- If you change parameters to fit history в†’ algorithm won’t work on new data

- Better a simple algorithm than an overfitted one

Keeping a journal:

Alongside the algorithm, it’s recommended to keep a trading journal — record why you entered a trade, why you exited, what emotions you felt. This helps identify behavioral patterns and improve discipline.

Risks of Algorithmic Trading

1. Technical Failure

Problem: Exchange down, internet lost, bot froze.

Example:

- Bot was supposed to sell at 5% loss

- Exchange didn’t respond for 10 minutes

- Loss: 20% instead of 5%

How to protect:

- VPS (virtual private server) near exchange

- Backup internet (4G + wired)

- Stop-loss on exchange (not just in bot)

2. “Black Swan”

Problem: Unpredictable event (exchange collapse, war, Elon Musk tweet).

Example:

- FTX collapse (November 2022)

- BTC dropped from $21,000 to $16,000 in a day

- Algorithms weren’t ready

How to protect:

- Diversification (not everything on one exchange)

- Position limits (no more 10% per asset)

- Manual control during crisis

3. Overfitting

Problem: Algorithm works perfectly on history, but not on real data.

Example:

- Backtest: +500% per year

- Reality: -50% per month

How to protect:

- Test on different periods (bull, bear, sideways)

- Don’t change parameters after every losing trade

- Use out-of-sample data (didn’t participate in optimization)

4. Competition

Problem: Other algorithms are faster, smarter, with more capital.

Example:

- Arbitrage opportunity disappears in 100ms

- HFT fund makes it, retail trader doesn’t

How to protect:

- Choose niches where HFT is ineffective (long-term strategies)

- Use unique data (alternative sources)

- Focus on risk management, not speed

Tools for Algo Trading

For Beginners (No Code)

- Veles: Cloud bots, backtests, simple interface — try Veles (affiliate link)

- Gainium: Grid, DCA, market making (free up to 2 bots)

- 3Commas: DCA, Grid, Trailing

- Cryptohopper: Ready strategies, marketplace

- Antbot: Signals, copy trading

- TradingView: Signals, alerts, Pine Script (gold standard for visual backtesting)

Algo Trading Platforms Comparison

| Platform | Type | Difficulty | Cost | Crypto | Forex/CFD | Backtests |

|---|---|---|---|---|---|---|

| Veles | Cloud | ⭐ | Free | ✅ | ❌ | ✅ |

| Gainium | Cloud | ⭐ | Freemium | ✅ | ❌ | ✅ |

| Ginarea | Cloud | ⭐⭐ | Freemium | ✅ | ✅ | ⚠️ Partial |

| 3Commas | Cloud | ⭐⭐ | $20-100/mo | ✅ | ❌ | ⚠️ |

| TradingView | Web | ⭐⭐ | $0-15/mo | ✅ | ✅ | ✅ |

| MT4/MT5 | Desktop | ⭐⭐⭐ | Free | ❌ | ✅ | ✅ |

| Python + CCXT | Code | ⭐⭐⭐⭐ | Free | ✅ | ❌ | ✅ |

| QuantConnect | Cloud | ⭐⭐⭐⭐⭐ | $0-1000/mo | ✅ | ✅ | ✅ |

Difficulty: ⭐ Very Easy | ⭐⭐⭐⭐⭐ Requires Programming

For Advanced (Code)

- Python + CCXT: Library for exchanges (free)

- Backtrader: Backtesting (free)

- Freqtrade: Open-source crypto bot (free)

For Pros

- QuantConnect: Platform for quants ($0-1,000/month)

- Interactive Brokers API: Traditional markets (commissions)

- Own infrastructure: Servers, direct connection (expensive)

Summary

Algorithmic trading — using rules for automated trading. From “caveman’s stick” to AI bots.

Main rules:

- Simple algorithm is better than complex

- Test on history, but don’t over-optimize

- Risk management is more important than returns

- Algorithm doesn’t replace thinking, it enhances it

Who algo trading is for:

- вњ… Traders who want to automate routine

- вњ… Investors for DCA and rebalancing

- вњ… Developers who love code + finance

Who it’s NOT for:

- вќЊ Expecting a “money button” (algorithm is a tool, not magic)

- вќЊ Not ready to learn (code, statistics, risks)

- вќЊ Want 100% guarantees (they don’t exist even with algorithm)

FAQ

Do I need to know how to code?

No. There are ready platforms (3Commas, Cryptohopper). But coding gives more flexibility and control.

How much capital do I need?

From $100 for DCA/Grid. From $1,000 for trend strategies. From $10,000 for arbitrage.

Can I make a living from algo trading?

Theoretically yes, but it requires capital of $100,000+ and returns of 10-20% annually. For most, it’s a supplement to main income.

Important: For retail traders with small capital ($1k-10k), trying to “make a living from it” immediately may lead to excessive risk and loss of deposit. However, you can start with a small amount, gradually grow your deposit, and build capital through profit reinvestment.

What risk is acceptable?

No more than 1-2% of capital per trade. Maximum drawdown — 20% (after that, review strategy).

How to choose an exchange for algo trading?

Criteria: low fees (0.02-0.1%), high liquidity, API for bots, reliability (Bybit, Binance, OKX).

What is a backtest?

Testing a strategy on historical data. Shows how the algorithm would have performed in the past. Doesn’t guarantee future results.

Can AI replace a trader?

AI is a tool, like a calculator. It doesn’t replace thinking, but speeds up analysis. Final decision is still up to the human.

Disclaimer

This blog is for informational purposes only. It does not constitute financial or investment advice.

Trading cryptocurrencies and other financial instruments involves high risk. You may lose all your funds.

The author is not responsible for any financial losses resulting from the use of information from this blog.